複雑さを乗り越え、ESG戦略の統合を推進し、組織に長期的な価値を付加します

急速に変化する今日の世界では、持続可能性は、特に建築環境において大きな重要性を増しています。建築環境は世界の炭素排出量の推定40パーセントを占めており、2050年までに気候変動の最悪の影響を緩和するために気温上昇を1.5℃の閾値に制限するためには、不動産の急速な脱炭素化が不可欠です。.

企業が持続可能性と責任ある事業慣行の重要性をますます認識するにつれ、組織において変化を推進し、複雑な状況を乗り越え、環境・社会・ガバナンス(ESG)のあらゆる側面における真の可能性を引き出すための、最高サステナビリティ責任者(CSO)またはサステナビリティ責任者の必要性が高まっています。この役割自体は新しいもので、CBREと米国グリーンビルディング協会が最近実施した調査では、601億3千万件以上の回答者が、この役割はここ3年間で初めて創設されたと述べています。.

サステナビリティ(ESGと同義に用いられることもあります)は、気候変動や人権から取締役会の多様性やコーポレートガバナンスに至るまで、非常に幅広い問題を包含しています。報告要件やコンプライアンス要件の厳格化、ステークホルダーからの圧力の高まり、気候変動リスクの軽減と適応、そして急速な技術革新といった、規制・法制度の急速な変化が、ESGの世界をますます複雑化し、その対応を困難にしています。.

したがって、CSO(またはサステナビリティ責任者)は、複雑な状況に対処し、ESG の考慮事項を組織の全体的な戦略に統合し、組織に継続的な価値を付加するための意思決定においてサステナビリティが不可欠な要素となるようにする上で重要な役割を果たします。.

アジア太平洋地域では、投資家が持続可能なポートフォリオへの関心を高め、テナントが自社のネットゼロおよびサステナビリティへのコミットメントに沿ってエネルギー効率が高く健康的な建物を求める中で、CSOの役割が急速に重要性を増しています。サステナビリティに関する情報開示を義務付ける新たな規制が増えるにつれ、CSOの役割はますます重要になり、APAC地域では人材獲得競争が激化しています。.

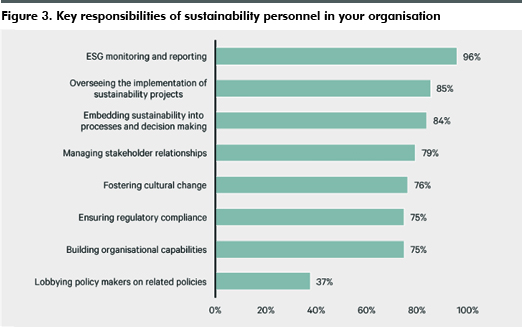

では、CSO にとって優先すべき焦点領域は何でしょうか? CBREと米国グリーンビルディング協会がアジア太平洋地域の67名以上の建築環境最高サステナビリティ責任者を対象に実施した最近の調査では、 , 回答者は、その権限は広範囲に及ぶと述べており、主な責任として、ESG の監視と報告 (96%) の実施、持続可能性関連のプロジェクトの実施 (85%) が挙げられています。.

CSOは、投資家、顧客、従業員、地域社会などのステークホルダーと組織との橋渡し役としての役割をますます重要にしています。社内においては、様々な部門と連携し、サステナビリティに関する取り組みを策定・実施し、イノベーションと効率性向上の機会を特定し、組織能力を構築する必要があります。.

調査回答者の84%(84%)が、ステークホルダーとの関係管理と文化変革の促進(76%)を自らの役割の重要な要素として挙げています。社内外のステークホルダーの懸念や期待に応え、透明性の高いコミュニケーションチャネルを構築・維持する必要があります。.

CSOはまた、将来の規制変更や、気候関連災害がポートフォリオに及ぼすリスクの理解がまだ初期段階にあることへの懸念も示しました。持続可能性の導入が企業ブランディング、人材獲得、気候リスク軽減にもたらす長期的なメリットを促進するためには、より多くの取り組みが必要であることを認識しています。持続可能性を根付かせるには、時間、優れたビジネス感覚、ステークホルダーマネジメント、そして人、地球、そしてビジネスパフォーマンスが相互に依存していることを認識し、前向きな変化を起こそうという強い意志が必要です。.

CSOはESGプロジェクトの進捗状況を追跡し、透明性を高めるという幅広い権限を持っている。

持続可能性関連の情報開示規制の強化を受けて、CSO の主な焦点は ESG の監視と報告、および関連プロジェクトの実施となっています。.

CSOは、企業のESG目標を推進し、それに沿った企業変革を促進する責任も負っています。これには、様々な事業部門がESG能力と説明責任を強化できるよう支援することも含まれます。.

多くのCSOは企業内部の優先事項の実施に重点を置く傾向があるため、関連政策について政策立案者へのロビー活動に取り組んでいるCSOは比較的少ない。しかし、脱炭素化への道筋には大幅な規制変更と政策支援が必要となるため、CSOにとってこれは見逃せない分野である。.

CBREでは、初代最高サステナビリティ責任者であるロブ・バーナード氏のリーダーシップと明確な方向性のメリットを目の当たりにしてきました。バーナード氏は昨年CBREに入社し、サステナビリティ、ビジネス、テクノロジーの交差点で20年間の経験を積み、マイクロソフト社の初代最高環境ストラテジストも務めました。彼のリーダーシップの下、CBREはグローバル事業全体におけるサステナビリティの統合を推進し、お客様により良いサービスを提供することで、2040年までにネットゼロカーボンを達成するというコミットメントの達成に貢献しています。私たちは、複雑さを簡素化し、明確で実行可能な戦略を通じてお客様にとってのサステナビリティの推進を加速させる体制を整えています。私たちは、規模の大小を問わず、グローバル、地域、そしてローカルを問わず、あらゆるお客様に対してこれを実現しています。.

私たちは、持続可能な未来に向けて、大規模な変化を推進し、業界を変革する力を持つツール、パートナーシップ、テクノロジー、そしてサービスに多大な投資を行ってきました。また、建築環境における持続可能性を推進するためには、クライアントが直面しているまさに同じ課題に取り組むことから、私たちの取り組みは私たちの家から始まると認識しています。.

CSOの役割は、サステナビリティの成熟に伴い進化を続け、この役割に投資した組織は、リスク管理、コスト削減と業務効率の向上、ステークホルダーとの連携、イノベーションの促進、従業員エンゲージメントの促進において、より優位な立場を築くことができます。CSOは多面的な役割を担い、組織のあらゆる部門に影響を及ぼします。これは、脱炭素社会への移行において競争優位性を獲得するために必要な抜本的な変化を反映しています。CSOの役割は、長期的な価値の創造、ブランドレピュテーションの向上、そして組織をサステナビリティとESGの実践におけるリーダーとして位置付ける上で極めて重要です。.

デビッド・フォガティ

シンガポールおよび東南アジアのサステナビリティ&ESGコンサルティングサービス責任者CBRE