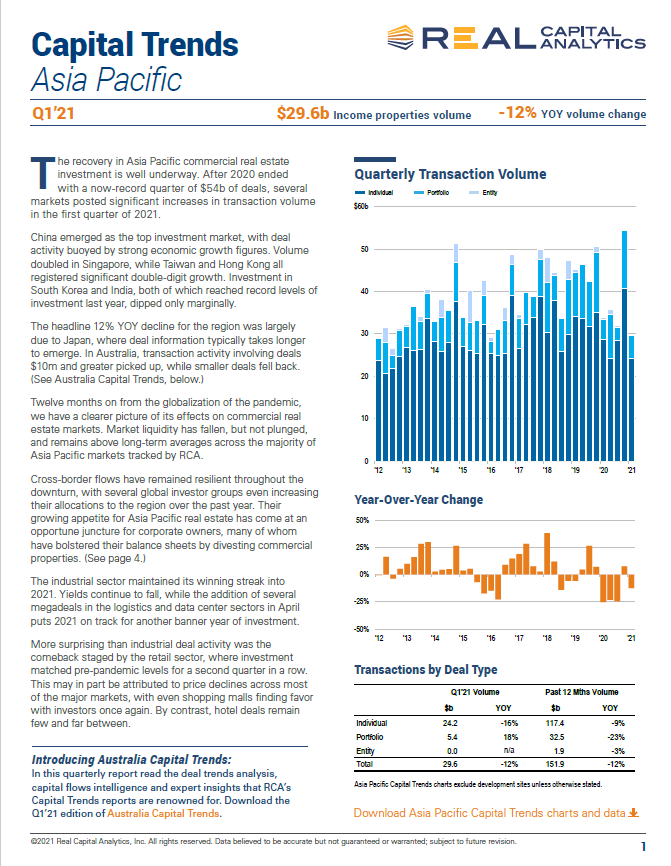

精彩片段

1. 破产事务上诉法院 NCLAT 在其最近的具有里程碑意义的裁决中,摧毁了清算顺序中担保债权人之间债权人优先顺序的概念。.

2.与《公司法》下的清算不同,《破产法》下的清算顺序取决于担保债权人的选择,即在法典之外强制执行或将财产移交给清算财产。.

3.担保债权人选择放弃其担保权益时,担保债权人之间的细分分类无关紧要。.

4.这样的清算顺序也可能改善异议担保金融债权人在处置阶段的地位。.

概述

全球债券市场2021年开局惨淡,一季度投资者因此跌至2016年第四季度以来的最低点,同时,美国10年期国债基准上涨超80个基点。由于债券利率在三月一路攀升,达一年来最高水平,在疫情爆发前,任何跌势都不会持续太久。这主要得益于亚太股票市场投资者对估值过高的担忧。

从疫情中夺取最多的科技股在此次引发售股浪潮中首当其冲,尤其是受到中国股市在国内的反措施垄断影响。而投资基金Archegos Capital的崩盘也让金融股感到紧张,使得该股市下跌亿的资金。这也让亚太地产股指数总体股票基准。

亚太房地产上市公司股票

GPR/APREA综合上市房地产指数反弹1.8%,其中,澳大利亚地产股在合订预期的推动下,在亚太地区的增长中处于领先地位。澳大利亚经济在2020年最后一个季度的GDP增长预期,随着调控放宽,住宅价格也持续上涨。日本股票的表现也随之大盘,主要得益于其最大的恐慌,以及防疫放松措施对市场信心的提升。同时,中国股市的涨幅受到限制,前期支持政策力度将缩小,有初步显示中国经济复苏正在进一步提速。

继合并办公和零售REITs之后,凯德集团紧接着又宣布一项企业重组计划,将其开发部门封闭,将其投资管理部门独立为专门的基金管理和创收业务。作为一家独立上市的公司,凯德投资管理将成为亚洲资产管理规模最大的房地产投资管理公司,以及全球第三大上市房地产投资管理公司,创立布鲁克菲尔德资产管理与百仕通。

亚太房地产投资信托基金

亚太REITs三月份上涨1.9%,地区主要市场普遍上行。除澳大利亚信心和工业信托表现强劲外,日本REITs也凭借其住宅REITs表现强劲,使得该版块在3月份亚太地区最高回报率。由于缺乏推动收益增长的规模,零售和酒店业失去增长势头。

与此同时,在房地产恐慌Filinvest向防疫证券交易所有关部门注册募股后,不到一年,防疫已准备推出其支REIT。该REIT第三主要由Filinvest发展的某商业区业务流程办公资产组成,如果允许超额配售,则此次爆发预计能募集149亿比索。

自去年底以来,投资逐步恢复活力,新加坡上市REITs重新积极寻找投资边境资产的机会,并于今年第一季度完成25亿美元的交易量,收购总额赶超去年。与此同时,丰树物流信托首次进军印度,以大约8440万新元的价格收购了位于普纳的仓库。腾飞REIT筹集了最大的边境资产,贡献超17亿美元,其中包括腾飞REIT在欧洲收购的首个数据中心。

前景展望

在疫情爆发一年后,亚太地产股已从三月低潮中强势反弹。但亚太房地产投资信托基金表现显着带动大盘房地产指数,为投资者带来接近38%的回报率,尽管仍落后于亚太股市。

由于基数效应放大预期,短期内经济前景仍存在不确定性。再加上由于变量病毒导致病例数量激增,无疑也为未来增加了更多的不确定性。供给必然和大宗商品价格上涨将着持续不平衡,甚至是面对经济复苏的混乱,投资者将继续债券上涨和政策收紧带来的影响。

然而,亚太REITs所提供的差距仍然可观,在一些发达市场通常能接近200个基点,甚至更高。随着经济活动常态化,持续的通货再膨胀贸易或与全球经济复苏同步保持一致。REITs无疑将在这一背景下进一步增长。如果在经济小区回升的前提下,压力卷土重来,那么就需要权衡彼此间的利弊。

概述

2021年伊始,全球债券市场遭遇重创,经历了自2016年第四季度以来投资者最糟糕的季度之一,10年期美国国债基准收益率飙升超过80个基点。然而,任何回调都昙花一现,债券收益率在3月份继续攀升,并在疫情爆发前达到一年多来的最高水平。收益率的飙升也给该地区的股市带来了压力,投资者对过高的估值感到担忧。.

疫情期间受益最大的科技股遭遇了抛售潮,这在很大程度上得益于中国政府对其本土反垄断行为的打击。此外,投资基金Archegos Capital的倒闭也令金融股受到冲击,该板块面临数十亿美元的损失。这推高了该地区房地产股的表现,使其超越了整体股票指数。.

上市房地产

GPR/APREA上市房地产综合指数回报率为1.8%,其中澳大利亚房地产股领涨该地区,主要得益于其捆绑式信托基金的强劲表现。随着限制措施的放松,澳大利亚经济在2020年第四季度公布了超出预期的GDP增长,住宅价格也持续上涨。日本股市也表现出色,这主要得益于其大型开发商的强劲表现,而紧急措施的解除提振了市场情绪。与此同时,由于投资者预期政策支持力度将会减弱,且经济复苏迹象进一步增强,中国股市涨幅受到限制。.

继办公楼和零售房地产投资信托基金合并之后,凯德集团宣布进行公司重组,将其开发部门私有化,并将其投资管理部门剥离出来,使其成为一家专注于基金管理和费用收入的纯粹业务公司。这家独立上市的公司——凯德投资管理有限公司——将成为亚洲最大的房地产投资管理公司(按资产管理规模计算),并位列全球第三大上市房地产投资管理公司,仅次于布鲁克菲尔德资产管理公司和黑石集团。.

房地产投资信托基金

亚太地区房地产投资信托基金(REITs)3月份上涨1.91万亿美元,主要市场普遍上涨。除了澳大利亚多元化和工业信托基金的强劲回报外,日本房地产投资信托基金(J-REITs)也受益于住宅房地产投资信托基金(Residential REITs)的强劲表现,推动该板块在3月份创下亚太地区最高回报率。由于缺乏进一步上涨的催化剂,零售和酒店板块的上涨势头有所减弱。.

与此同时,菲律宾有望在不到一年的时间内推出第三只房地产投资信托基金(REIT)。开发商菲利宾投资公司(Filinvest)已向该国交易所提交了发行申请。该REIT主要包含菲利宾投资公司在其总体开发的商业区内的BPO办公资产,如果超额配售选择权被行使,预计将筹集149亿菲律宾比索。.

随着去年底投资活动强劲复苏,新加坡上市的房地产投资信托基金(REITs)继续保持着跨境资产收购的势头。继第一季度达成100万亿美元(1000亿至4万亿美元)的交易后,该行业的收购总额有望超过去年同期水平。值得注意的是,丰树物流信托首次进军印度市场,斥资约8440万新加坡元(1000万至4万亿美元)收购了位于浦那市的两处仓库。腾飞房地产投资信托基金(Ascendas REIT)是最大的投资方,投资额超过17亿美元(1000万至4万亿美元),其中包括该信托基金在欧洲的首批数据中心收购。.

前景

疫情爆发一年后,亚太地区的房地产股票已从3月份的低点强劲反弹。尽管该地区的房地产投资信托基金(REITs)表现显著优于整体房地产指数,为投资者带来了接近38%的回报,但它们仍然落后于亚太股市。.

短期前景仍将波动,基数效应会放大通胀预期。此外,近期新病毒变种病例激增无疑会加剧未来的不确定性。鉴于供应短缺的阴影和商品价格上涨预示着经济复苏将持续进行,尽管过程可能不均衡且有时混乱,投资者将继续应对债券收益率上升以及政策收紧带来的影响。.

尽管如此,该地区房地产投资信托基金(REITs)提供的利差仍然可观,通常接近200个基点,在一些发达市场甚至更高。随着经济活动逐步恢复正常,持续的通胀交易可能与全球经济同步复苏相一致。毫无疑问,REITs将受益于此,进一步推高价格。而通胀压力的回归,如果能够有序进行,则是不可避免的权衡。.

尽管关于未来职场仍存在诸多疑问,但越来越明显的是,将办公室视为唯一的工作场所这一观念已不再适用,实际上存在一种 工作场所生态系统.

设施管理(FM)需要相应地进行调整和演进。企业办公场所的管理方式已经发生了变化;这种变革性做法需要持续推进,并很快扩展到办公场所之外的其他场所。.

基于我们在全球范围内的集体经验——包括通过反复实践总结出的最佳实践、为客户实施的解决方案,以及收集和分析的数据——我们识别出设施管理领域在以下三个核心领域中发生了哪些重大变化、出现了哪些新兴趋势,以及未来的发展方向:

对主要以公共交通为导向的基础设施项目及其关键影响市场的全面分析

班加罗尔是印度主要的经济增长引擎之一。该市贡献了卡纳塔克邦国内生产总值的三分之一以上,也是该邦创造就业机会的主要动力。 除了拥有’印度IT之都”这一久负盛名的称号外,如今它已成为印度的“创业之都”和领先的金融科技中心。 鉴于巨大的经济机遇、就业岗位的创造以及预计人口将从2011年的1169万增长至2021年的1648万, 班加罗尔大都市区(BMR)的基础设施和公共服务亟需扩建与升级,这一需求从未像现在这样迫切。尤其是城市交通基础设施。.

《2020年班加罗尔城市基础设施报告——对主要交通导向型基础设施项目及关键影响市场的全面解读》深入剖析了上述交通基础设施项目。该报告从需求增长将带动房地产市场活跃度的角度出发,分析了这些项目对房地产市场的影响。 我们探讨了监管干预措施、规划交通基础设施的系统性实施,以及城市有机发展所发挥的作用。尽管关于城市基础设施的讨论已超越交通范畴,延伸至影响环境可持续性、空气和水质等其他因素,但交通基础设施仍是影响房地产市场的关键因素。.

Kemmu Kawai 于 2022 年 9 月加入 Longevity Partners Japan,担任国家总监。他常驻东京,负责日本、亚太地区及其他地区的所有业务和活动。他拥有超过 16 年的金融从业经验,专门从事房地产和信贷投资。在加入 Longevity Partners 之前,他曾在 Norinchukin 银行担任投资组合经理,并在 Center Point Development 担任投资经理。.

Kemmu Kawai

常务董事

长寿伙伴