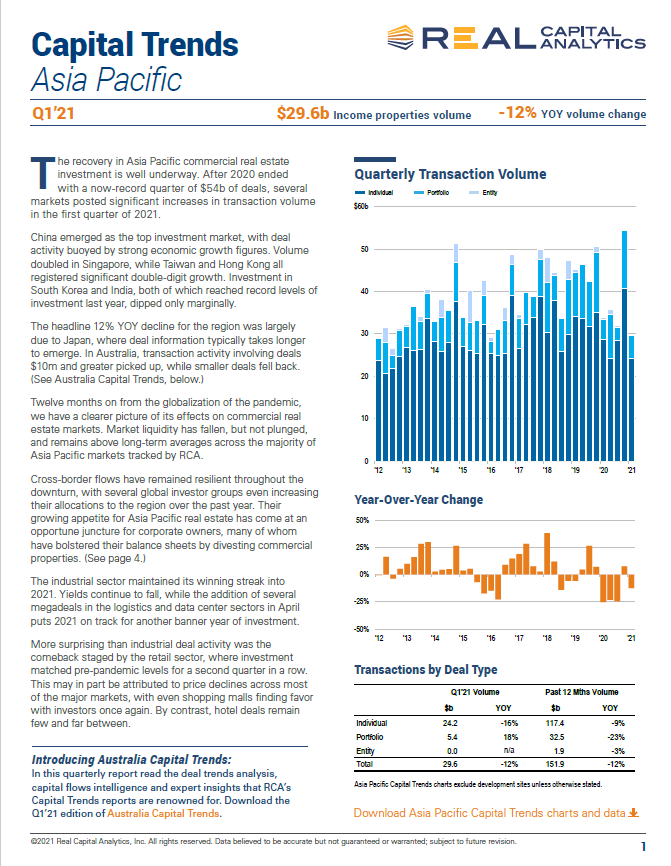

The COVID-19 pandemic brought the logistics sector abruptly into the global spotlight. With increased attention on the sector, both in 2020 and in the near-term, this report focuses on key drivers for the sector, recent market performance and an outlook for the industry.

Growth drivers

- At the ground level, ongoing population growth and economic expansion will drive the global middle class almost to double over the next decade. This increased level of consumption, together with the accelerated shift to e-commerce, will fundamentally drive the need for stronger, more resilient and more diverse supply chains. Ongoing development of transport infrastructure will be critical to ensure market connectivity.

- A shortage of labor in some markets, especially across Europe, together with a sharper focus on Environmental, Social and Governance (ESG) priorities, will force accelerated adoption of technology to bring greater efficiencies and transparency. Similarly, the use of third-party logistics (3PL) operators will continue to grow as they provide corporations with opportunities for greater nimbleness and flexibility in meeting consumer demand.

- Geo-politics will continue to shape the global trade environment. Many short-term interim solutions have been put in place to safeguard against recent trade flow disruptions, but complete roll out of new supply chain solutions will take years as corporates weigh opportunities for reshoring and demand/supply drivers.

Leasing Market

- Industrial markets have proved resilient in 2020, and demand remained robust, despite economic growth figures being amongst the worst on record. Accordingly, industrial/logistics vacancy has remained tight across the world, although this has been due, in part, to limited development supply pipelines.

- Notwithstanding, rental growth has remained comparatively elusive across the world with less than half of the markets tracked recording growth in 2020 but this varies in and within regions. While this may not be surprising in light of the pandemic, it also reflects the longer-term stagnation in rents, with less than half of the global markets having achieved more than 2.5% rental growth per annum since 2017. However, this is expected to change with increased cost pressures being exerted on landlords; not least of all being higher acquisition costs and increased land taxes and infrastructure charges.

Outlook

- Demand drivers highlight gaps in supply chains that can potentially be addressed by the expanded range of logistics asset types. To the extent supply chains connect production to consumption, these gaps can be in the same or across multiple regions.

- Structural trends fueling demand over the long-term are also being accelerated by both business and consumer reactions to the pandemic. The investor outlook, therefore, is continued strong capital and income returns, with the latter likely to increase in contribution.

- The combination of strong demand and supply chain reconfigurations to enhance efficiencies puts a sharper focus on land availability for new development. This will be a fundamental issue that needs to be addressed for real estate to meet the future needs of the sector.