Asia Pacific Leasing Market Sentiment Index (CBRE)

CBRE’s latest leasing market sentiment index reveals that regional leasing sentiment is improving amid a rise in enquiries:

Tenant enquiries and site visits registered an increase over the surveyed period. Leasing enquiries and inspections remained strong, led by retail.

While expansionary demand continued to strengthen across the retail sector, there was a slight weakening in requirements for office and industrial space.

More than half of the respondents believe that rents and incentives will remain flat. The remaining respondents were divided between those having a positive outlook for Singapore and Korea and those expecting a rental decline in Greater China.

Most major markets reported stronger leasing sentiment. Sentiment in Japan entered positive territory for the first time since 2020, while both Hong Kong SAR and Australia saw sentiment rebound from negative territory. Mainland China was the only market to witness negative sentiment, indicating that this market will require more time to recover.

As the world continues to transition, companies are asking themselves how they can contribute, lower the effects of climate change, and bring meaningful value into the lives and communities in which they operate. Here at KIC we build and manage logistics centers, and we ask ourselves those questions during our entire process. From finding the correct building site, to the construction of the logistics center, all the way down to finding the best tenants and managing the property. Here is how energy generation and energy management are being used in our facilities to help bring about a low carbon future.

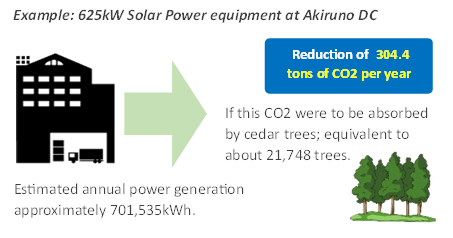

Energy Generation (PPA Application)

Construction and retrofitting buildings with more energy efficient features is becoming a common practice and an important factor to tenants. Logistics facilities can be power hungry structures especially those with cold storage and large rooftops. Therefore, it is important for builders and management companies to continue to apply new energy technology.

Solar energy and power purchase agreements (PPA) are perfect examples of how a logistics facility can implement new energy technology to help lower its carbon dioxide emissions. With a power purchase agreement (PPA), a third party installs a solar power generation system on the roof of the logistics building and supplies the generated electricity to the tenants. This allows the tenants to use green energy, lowers their electricity rates compared to conventional electricity and provides them with power even in the event of a disaster.

Energy Management

In addition to energy generation technology, energy management is also a very important factor in lowering electricity consumption and the overall carbon footprint of the facility. Energy management increases efficiency and limits the waste of power. For example, saving energy by switching to LED lights. LEDs consume less power and have a longer life span. The power consumption of LED is about 20% of incandescent bulbs, 30% of fluorescent bulbs and 25% of mercury lamps. It significantly reduces the electricity bill and lasts about 10 years. As a result, fewer electric lights are thrown away and labor cost of switching light bulbs is reduced.

Conclusion

Overall, energy generation and energy management are important to tenants and investors. Simple solutions such as switching to LED lights are available as well as more complicated ones such as solar power rooftops and large capacity rechargeable batteries. As we continue forward, it is important to keep in mind that green energy solutions are already making their way into logistics real estate.

Asia Pacific Trends Q3 2023 features in-depth and up-to-date data and insights on the Office, Retail, Industrial & Logistics and Investment markets across the region. Key trends include:

Office:

Leasing demand remains weak as occupiers stay cautious

Mainland China, India and Tokyo account for bulk of activity

Transactions take longer to close due to slow approvals

Non-banking financial and tech firms drive demand

Most markets set to remain in favour of tenants

Retail:

Retail sales moderate but travel demand continues to provide strong tailwinds

Retailers stay in expansion mode; Location remains key as demand focuses on prime locations

Consumer demand for unique experiences drives leasing for non-traditional retail space

Japan remains most upbeat market thanks to strong tourist inflows

Leasing demand projected to remain robust in coming quarters

Industrial & Logistics:

Slowing regional economy continues to weigh on leasing activity

Strong demand from ecommerce platforms and stable activity from 3PLs

Supply pipeline remains significant

Investment volume holds steady in the first three quarters of the year

Leasing and investment volume forecasted to soften

Investment:

Sentiment remains weak despite slight uptick in investment volume

Re-pricing continues to constrain purchasing activity

Retail and hotel assets witness stronger deal flow

Japan remains most upbeat market

Investment to stay subdued amid high interest rate environment

As experts in commercial real estate, our work is built on successfully identifying and navigating opportunities for our clients. In our fourth annual Global Investor Outlook report, we provide a comprehensive, in-depth look at the trends set to dominate the investment market and where we think opportunities can be found in the year ahead. We have synthesised views from our senior Capital Markets experts and investors around the world.

In 2024, challenging conditions will persist, but a clearer rate outlook and tightening bid-ask spreads appear to be on the horizon. As investors continue to seek stability in policy environments, the industrial & logistics (I&L), multifamily and office sectors largely remain their top picks in the upcoming year. As momentum builds, the best-positioned investors will be those who are ready to act on opportunity.

Global Key Themes

Real estate assets retain appeal despite ‘higher for longer’ interest rates. Pricing will continue to adjust to a more realistic equilibrium, and we expect transactions to pick up in H2 2024.

Pockets of opportunity are continuing to emerge under tighter conditions. Property funds are facing redemption pressures, and a higher cost of capital is seeing more owner occupiers unlock capital via sale and leaseback transactions.

A calmer rate environment is coaxing out capital. We anticipate investors will begin to deploy capital that is primarily opportunistic or value-add led on a selective basis.

Investors continuing to flock to I&L assets due to their perceived stability and growth potential. Investors are migrating to related sub-sectors such as cold/dark storage.

Number of alliances are growing as investors look at different opportunities to pool resources and mobilise funds. The complexity of accessing some specialised assets such as student housing and data centres will drive more partnerships and joint ventures between investors and developers.

Growing acceptance of ESG as a key element of investment decision-making. A record proportion (25%) of investors surveyed have ESG-based disposal and acquisition strategies in place, particularly in EMEA and APAC – up from 10% just two years ago. We expect a wave of disposals and value-add opportunities to enter the market.

Rebounding Asia Pacific: Conference Takeaways from the Asia Pacific Real Assets Leaders’ Congress 2023

Read the highlights and takeaways from APREA’s flagship conference, the Asia Pacific Real Assets Leaders’ Congress 2023, which featured the best and the brightest in the industry.

Despite global challenges, optimism prevails for Asia Pacific’s growth, presenting opportunities in both public and private markets. Key takeaways include the region’s commitment to sustainability driving investment opportunities, discussions on infrastructure financing challenges and opportunities, insights into traditional vs alternative assets, the impact of rising interest rates on REITs, and the evolving landscape of family offices.

The Business Case of Embracing ESG – A CDL Case Study

2023 is set to be the hottest year since records began in the mid-1800s. The Swiss Re Institute further warns that without climate action, the world economy could shrink by 18% in the next 30 years. Asian economies are particularly vulnerable – with China at risk of losing almost 24% of its GDP under the most severe climate scenario. In contrast, these figures can lessen and be as low as 4% if the 2015 Paris Agreement targets are met.

The cost of inaction is greater than the cost of action. With societal demands for ethical and responsible business practice intensifying, consumers, investors, and employees are increasingly scrutinising companies’ ESG (environmental, social and governance) performance, favouring those that prioritise environmental stewardship, social responsibility, and sound governance.

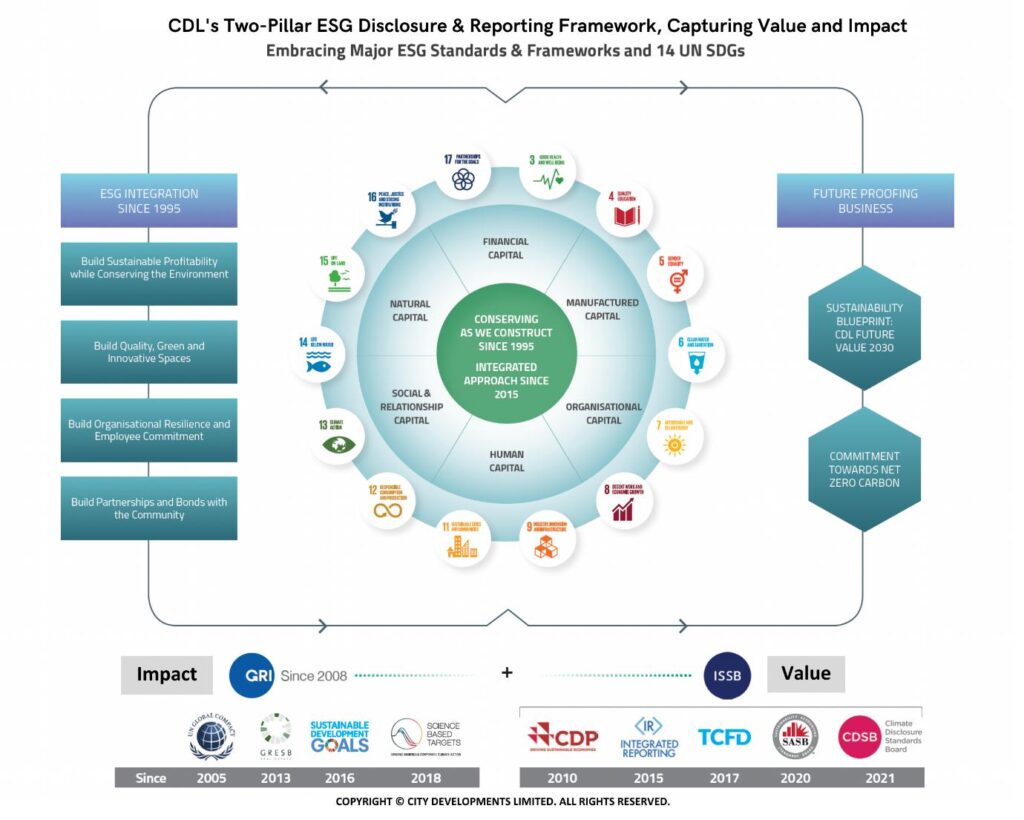

City Developments Limited (CDL)’s ESG strategy and firm commitment to “Conserving as We Construct”, established in 1995, has positioned the company well in the transition towards sustainable business operations. Its value creation business model anchored on four key pillars — Integration, Innovation, Investment, and Impact – provides the company with a solid foundation to mitigate and adapt to unprecedented threats and challenges. With long-standing board and leadership commitment and stakeholders’ support, CDL has remained effective in achieving three deliverables: “Decarbonisation”, “Digitalisation and Innovation” and “Disclosure and Communication”.

Integrating Sustainability into a Company’s Governance Structure, Strategy and Operations

In 2012, CDL established a dedicated Corporate Social Responsibility (CSR) and Corporate Governance comprising independent directors, to provide strategic direction and oversight of its ESG activities. In 2016, the committee was renamed Board Sustainability Committee. The committee ensures that ESG considerations are embedded within CDL’s corporate strategy and decision-making processes.

CDL’s integrated sustainability governance structure that extends both horizontally between the ESG pillars and functions and vertically across hierarchical levels up to the Group CEO and the Board

Effective corporate governance includes putting in place essential policies and guidelines across the organisation. To enhance transparency, CDL’s corporate policies and guidelines are publicly available on its corporate website, sustainability microsite and staff intranet.

Innovation and Investment: Harnessing Green Technologies and Sustainable Financing

Climate and social risks are business and investment risks. As demand for green financing grows, companies with strong ESG performance will gain better access to fast-growing ESG investment funds. In 2022, CDL established its Sustainable Investment Principles to govern ESG factors in investment decisions, aligning CDL’s investments with its commitment towards a low-carbon future.

Building a green and low-carbon future is not possible without smart and innovative solutions. In 2020, CDL set up Green Building, Decarbonisation and Safety team to play a pivotal role in driving innovation and investment. The team identifies and implements cutting-edge technologies and solutions to reduce CDL’s carbon footprint in construction, operations, and asset management.

Impact: Setting targets, tracking, and disclosing ESG performance

Companies can only manage what they measure. As the first Singapore company to publish a dedicated sustainability report since 2008, CDL has benefitted from the hands-on experience of producing 16 sustainability reports to-date. Using a unique blended reporting model harmonising key and relevant international reporting frameworks, standards, and approaches with the GRI Standards at its core, CDL has been able to identify material issues, set targets, track performance, and improve deliverables. This has enabled its management to take strategic and prompt action to improve, generate positive impacts and future-proof its business.

CDL’s Value Creation Model, a unique blended two-pillar sustainability reporting framework that harmonises nine key ESG reporting standards and 14 UN Sustainable Development Goals

Looking ahead, the global race to zero will continue to exert pressure on countries and companies to accelerate climate action. Sustainability-related risks and opportunities will likely increase as social, political, and cultural attitudes continue to evolve. The integration of ESG into a company’s corporate strategy is thus critical for sustained value creation.

CBRE professionals in Asia Pacific observe that investor risk appetite remains low amid a delayed recovery in investment activity. A majority of respondents expect a recovery from Q2 2024 onwards, amid limited expectations of interest rate cuts in the first half of 2024.

Selling pressure persists across most of the region, with the primary exception of India which is receiving increased buying interest from investors. Most investors – excluding private investors and institutional investors/LPs – also have higher intentions to sell than in Q1 2023.

The survey reveals that the price gap is widening for assets with strong fundamentals, such as multifamily, institutional-grade modern logistics facilities, prime shopping malls, cold storage and data centres.

While institutional-grade logistics remains the most popular sector for investors, interest in retail has increased. Slow re-pricing is prompting investors to seek alternative or niche sectors, with real estate debt strategies gaining traction among alternatives.

Cap rates are set to expand across Asia Pacific, reflecting a prolonged high interest rate environment, and as re-pricing lags behind the US and Europe.

Asia Pacific Glide Path Report (Cushman & Wakefield)

What we know is that the global commercial real estate (CRE) sector, like many sectors, faces significant near-term headwinds. In Asia Pacific, while the economy remains resilient, the CRE investment market is in the middle of a reset given interest rate uncertainty, tighter lending conditions, and a challenging global environment. However, we also know that the CRE sector will recover. In fact, historically, the strongest vintage years in terms of CRE returns are the ones that follow periods of dislocation and financial stress.

This report provides a glide path from here to there. That path will not be without challenge; it is therefore just as important to address the near-term challenges as it is to conceptualise the path to clear(er) skies. Our approach to investing is predicated in part on positioning for the future and not missing out on thematic and demographics that will drive Asia Pacific in the next decade.

Kemmu Kawai joined Longevity Partners Japan in September 2022 as the Country Director. Based in Tokyo, he oversees all operations and activities in Japan, the Asia-Pacific region and beyond. He brings him more than 16 years of experience in finance where he specialised in real estate and credit investments. Before joining Longevity Partners, he served as a Portfolio Manager at Norinchukin Bank and as Investment Manager at Center Point Development.