As the world continues to transition, companies are asking themselves how they can contribute, lower the effects of climate change, and bring meaningful value into the lives and communities in which they operate. Here at KIC we build and manage logistics centers, and we ask ourselves those questions during our entire process. From finding the correct building site, to the construction of the logistics center, all the way down to finding the best tenants and managing the property. Here is how energy generation and energy management are being used in our facilities to help bring about a low carbon future.

Energy Generation (PPA Application)

Construction and retrofitting buildings with more energy efficient features is becoming a common practice and an important factor to tenants. Logistics facilities can be power hungry structures especially those with cold storage and large rooftops. Therefore, it is important for builders and management companies to continue to apply new energy technology.

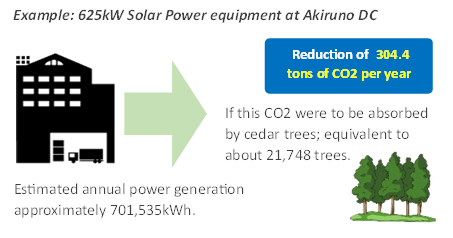

Solar energy and power purchase agreements (PPA) are perfect examples of how a logistics facility can implement new energy technology to help lower its carbon dioxide emissions. With a power purchase agreement (PPA), a third party installs a solar power generation system on the roof of the logistics building and supplies the generated electricity to the tenants. This allows the tenants to use green energy, lowers their electricity rates compared to conventional electricity and provides them with power even in the event of a disaster.

Energy Management

In addition to energy generation technology, energy management is also a very important factor in lowering electricity consumption and the overall carbon footprint of the facility. Energy management increases efficiency and limits the waste of power. For example, saving energy by switching to LED lights. LEDs consume less power and have a longer life span. The power consumption of LED is about 20% of incandescent bulbs, 30% of fluorescent bulbs and 25% of mercury lamps. It significantly reduces the electricity bill and lasts about 10 years. As a result, fewer electric lights are thrown away and labor cost of switching light bulbs is reduced.

Conclusion

Overall, energy generation and energy management are important to tenants and investors. Simple solutions such as switching to LED lights are available as well as more complicated ones such as solar power rooftops and large capacity rechargeable batteries. As we continue forward, it is important to keep in mind that green energy solutions are already making their way into logistics real estate.

Katsuyuki Victor Mineta

Founder & CEO

KIC Holdings