Overall: We still believe that the interest rate tailwind of slower global growth will support REITs in Asia especially Australia, Singapore and even Hong Kong (see fall in HIBOR). CPI in our region outside of Japan has been trending very much in the right direction.

Japan (+7% in USD in April): The major developers will publish their annual results in May. After that it will be quiet until October and we see only limited upside potential. We have therefore added to REITs and bought Japan Real Estate Investment Corp.

Australia (+9%): We continue to favor names like Stockland and Mirvac as we anticipate residential volumes to recover as the RBA cuts throughout the year. We are positive on self-storage due to continued population growth, and potential for more consolidation of unlisted, smaller players.

Hong Kong (+2.3%): Money market rates continue to fall, the 1M HIBOR is below 2% now. For the short-term refinanced companies in Hong Kong a strong tailwind.

Singapore (1.7%): We see continued drops in funding costs which will help earnings and fuel acquisition growth for some names that have strong costs of capital. With 1Q updates behind us, we see limited negative catalysts for the sector.

2050 Net-Zero: How Regional ESG Trends in Real Estate Are Driving Global Integration

The global real estate sector faces mounting pressure to decarbonise, contributing nearly 40% of total emissions (1). With the 2050 net-zero target fast approaching, investors and asset managers must urgently align with evolving ESG standards or risk falling behind.

Europe: Regulatory Leadership and Standardisation

Europe leads the way in ESG integration with rigorous regulatory frameworks. The EU Taxonomy for Sustainable Activities (2) provides a clear classification system for environmentally sustainable investments, guiding capital allocation towards green real estate. Additionally, the Global Real Estate Sustainability Benchmark (GRESB) (3)—originally developed in Europe—has become a widely accepted ESG performance measurement tool, shaping investment decisions worldwide.

GRESB’s influence extends beyond Europe, particularly into the Asia-Pacific (APAC) region, where a joint study with ANREV found that higher GRESB scores correlate with stronger financial performance. This has encouraged investors and developers across APAC to integrate sustainability benchmarks into asset management, enhancing ESG disclosures and compliance.

United States: Market-Driven ESG Adoption

Unlike Europe’s regulatory-first approach, the US real estate sector is driven by market incentives and investor demand. The Inflation Reduction Act (2022) promotes building efficiency and renewable energy adoption, while major cities have introduced stringent local policies. New York City’s Local Law 97 (4) mandates a 40% reduction in building emissions by 2030, penalising non-compliance with significant financial consequences.

Beyond regulation, major institutional investors such as BlackRock and Brookfield have embedded ESG principles into real estate portfolio strategies. The increasing willingness of tenants to pay a premium for energy-efficient spaces further highlights the market-driven shift towards sustainability.

Asia: Diverse Strategies Across Developed and Emerging Markets

Asia’s real estate ESG trends vary by region. China is focusing on large-scale sustainable urban developments as part of its 2060 carbon-neutral goal. Japan and South Korea are leveraging smart-grid technology and AI-driven energy management to improve efficiency and emissions tracking.

In Southeast Asia, where economies are still developing, international financial support is playing a crucial role in accelerating sustainability efforts. Singapore, for instance, has seen rapid growth in green-certified buildings, with investors aligning assets to Task Force on Climate-related Financial Disclosures (TCFD) (5) and Science-Based Targets (SBTi) (6) recommendations to improve transparency and global compliance.

A Global Shift Towards Sustainable Real Estate

Despite regional differences, ESG integration in real estate is becoming a global imperative. Investors, developers, and asset managers must navigate evolving standards while ensuring properties remain competitive in an increasingly sustainability-driven market.

To remain ahead, real estate leaders must proactively:

Conduct energy audits and efficiency upgrades

Invest in building retrofits and renewable energy integration

Align assets with globally recognised ESG benchmarks

As the real estate industry moves toward a net-zero future, those who embrace sustainability will protect long-term assett value and strengthen their market position. The shift from regional approaches to a globally integrated ESG strategy is already underway—now is the time for decisive action.

References:

1. International Energy Agency (IEA). (2022). Buildings Sector Energy Consumption and Emissions. Retrieved from: https://www.iea.org/topics/buildings

Trump 2.0—The First 100 Days: Implications for the Economy & Property (Cushman & Wakefield)

Trump 2.0—The First 100 Days explores the early economic and commercial real estate implications of President Trump’s 2025 policy agenda. Building on our analyses of the First 100 Days from the last two administrations, this series of reports examines critical developments in trade policy, tax reforms, immigration and other policy priorities. To provide tailored insights, we’ve created focused analyses for the U.S. and Canada, as well as the APAC and EMEA regions, highlighting the economic and property sector outlook in each area. Each report dives into relevant regional trends across sectors, offering invaluable insights for occupiers and investors navigating today’s landscape.

Our analysis presents the most probable and possible scenarios based on current data, but conditions remain dynamic, with new developments still emerging. Both potential opportunities and challenges may arise as these policies take shape over time.

Investing in the Philippines: Opportunities, Challenges, and the Road Ahead

The Philippines is emerging as a promising investment destination, driven by strong macroeconomic fundamentals, a dynamic consumer base, and expanding opportunities in REITs, hospitality, and renewable energy. Real estate diversification, sustainable development, and infrastructure upgrades are creating new growth avenues across both primary and secondary markets.

As global supply chains diversify, the country’s strategic location and young workforce further position it for long-term gains. Investors who navigate local dynamics carefully and prioritize sustainability and partnerships with experienced players stand to unlock substantial value.

The revitalisation and redevelopment of an asset is not just a straightforward renovation of the physical facilities of a property but can also be a chance to improve on sustainability, community engagement and cultural integration of the entire area. A thoughtful asset manager can also take the opportunity to rebrand and enhance its offerings through a renewed experience for its visitors.

Located along the Singapore River in the heart of the city, the recently transformed CQ @ Clarke Quay (CQ) bustles with excitement and entertainment with its myriad of retail and lifestyle experiences for locals and tourists alike. Offering options for both day and night, the area’s historical charm and modern amenities blend together seamlessly to provide a unique atmosphere.

Lesser known is that sustainable features have been incorporated into its redevelopment that not only have a positive impact on the environment, but also enhance wellness and comfort of the community.

Approximately 34% of its recent rejuvenation cost was allocated towards improving operational efficiency and integrating sustainable building features. Because of these enhancements, CQ’s green rating has been elevated from Green Mark Certified to Green Mark GoldPLUS, both green building ratings conferred by the Building and Construction Authority (BCA) in Singapore.

Existing angel canopies were upgraded with advanced ethylene tetrafluoroethylene (ETFE) membranes to increase thermal comfort.

Although naturally ventilated, visitors enjoy a comfortable stroll down the inner streets of CQ due to the upgraded angel canopies made with advanced ethylene tetrafluoroethylene (ETFE) membranes that optimise the entrance of daylight while also reducing solar heat gain by 70%. New omni-directional fans have been installed, lowering the environmental temperature by approximately 2°C through evaporative mist cooling while reducing energy consumption by approximately 50% compared to standard fans. CQ’s property management systems were enhanced, including the upgrade of the building chiller plant to attain a system efficiency of 0.60kW/RT.

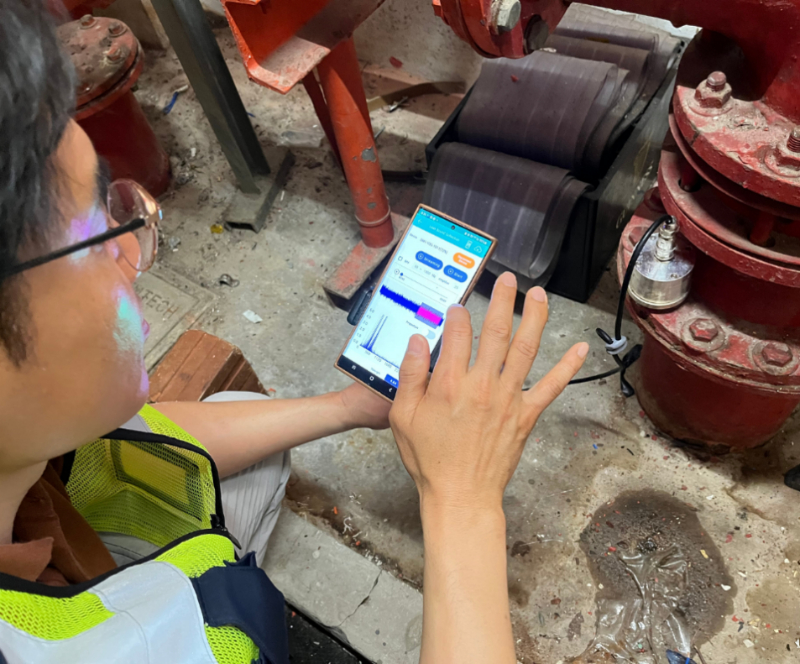

The WI.Plat technology is able to identify pipe leakages using an IoT sensor.

During the enhancement, the team took the chance to identify other rectification works required, including the detection of pipe leakages to prevent water loss and property damage. But with an extensive network of underground pipes beneath the historical structures, this process was complex and tricky. WI.Plat, a CapitaLand Sustainability X Challenge innovation, came in handy. It is a high-precision acoustic IoT sensor technology from Korea with a machine learning algorithm that identified otherwise difficult to locate underground pipe leaks.

Mural artwork by Yip Yew Chong and tobyato fronting Block B – The Warehouses

Many who visit CQ may not be familiar with its rich culture and legacy, including its past life as a major transshipment zone and a conduit for trade, where cargo from the tongkangs and twakows, historical cargo vessels, would be manually unloaded along the river. Seven warehouses were restored, preserving their godown typology while being adorned in new colours. Heritage jack roofs were reinstated and glass skylights incorporated to draw in natural light. The warehouse façades were painted with mural by local artists Yip Yew Chong and tobyato inspired by Clarke Quay’s heritage as a Teochew enclave. Upgraded steps doubling up as seats were added to the landing of Read Bridge, paying tribute to the Bridge’s historical role as a communal space, complemented by a new accessibility ramp incorporating upcycled wood pieces from the last two twakows. Furthermore, heritage panels and bronze plate tiles, strategically positioned throughout the area, recount the enthralling history of the Singapore River and Clarke Quay precinct, serving as educational elements for visitors as they explore the area’s rich heritage.

CQ has also been enhanced with modern and exciting offerings and new retail concepts. Fairprice Finest Clarke Quay offers products in collaboration with Singapore- based partners and its Grocer Food Hall offers “You Pick, We Cook” services as well as curated cocktails infused with local flavours. Swee Lee Clarke Quay is housed in an approximately 60% of repurposed warehouse unit housing an experiential and community space and pet-friendly amenities.

ESG in Real Assets: Balancing Digital Innovation, Sustainability, and Social Impact

As ESG adoption in real assets accelerates, identifying the right technology remains a complex challenge. There is no one-size-fits-all approach—ESG tools must align with a firm’s portfolio, investment strategy and data maturity. At the APREA Singapore Conference, industry experts emphasized the need for flexible, value-driven solutions.

For firms like SC Capital Partners, a private equity real estate firm managing over 60 assets across diverse classes in Asia-Pacific, agility and pragmatism in ESG strategy are essential. Unlike traditional developers with long-term investment horizons, SC Capital Partner follows an opportunistic investment strategy, where holding periods vary and assets may be divested ahead of schedule in response to market dynamics. This variability renders costly, rigid digital tools impractical, says Miak Ou, Director and Head of Sustainability at SC Capital Partners.

“Technology must align with a firm’s ESG maturity, portfolio strategy and data readiness,” says Ou. “What works for a long-term core asset might not necessarily work for an opportunistic investment with a short and unpredictable holding period.”

Firms should prioritize value-driven adoption over trends. SC Capital Partners, for instance, currently uses a structured Excel-based system – developed with consultants – as it is flexible, cost-effective, and well-integrated with current workflows. Rather than invest in proprietary tools, the firm integrates with operators’ existing digital platforms to reduce implementation risk and accelerate adoption.

The edge lies not in the tool itself, but in the ability to measure, analyse, and apply data to make better investment decisions. While digital tools enhance tenant and guest experiences, Ou notes that smart building technologies are especially impactful in sectors like co-living, student accommodation, and self-storage, where they drive operational efficiency. In hospitality, innovations like mobile check-ins and smart room controls prioritize personalization over full automation.

Among the panelists, Esther An, Chief Sustainability Officer at City Developments Limited (CDL) highlighted the importance of the built environment in contributing to a net zero carbon future. She shared how CDL has leveraged green building and energy-efficient technologies and practices to reduce operation costs without compromising on users’ productivity and comfort founded on its ethos of ‘Conserving as We Construct’ established in 1995. She pointed to rising carbon taxes and grid prices that will require businesses for deeper and greater sustainability integration and innovation. Digital tools are key to improving ESG data collation, analysis and reporting to meet the rising expectation of regulators, investors and financiers, she said.

“Applying AI to improve business operations is definitely a no-brainer,” An, said. “ The key is on how do you deploy it efficiently to achieve the desired impact? Over the past 10 years, we have been saving an average of $3 to $4 million a year thanks to the effective application of energy-efficient technologies and practices.” AI-powered facility management platforms have helped us to optimize resource use through reducing lighting, air conditioning, and manpower deployment in underutilized spaces. This approach extends to car parks and large-scale infrastructure, reducing costs and improving operational efficiency, she noted. Temperature and grid prices will continue to rise, AI and technologies application to improve performance will be critical to future-proof businesses.

The Social Pillar: A Growing Focus in ESG

While governance and environmental concerns often dominate ESG discussions, the social pillar—spanning diversity, well-being and community engagement—receives less attention. However, demand for human-centric real estate is growing, particularly in student housing and senior living. Investors and tenants increasingly prioritize inclusivity, mental well-being and social impact.

Real estate leaders must integrate social impact in ESG strategies to enhance community well-being, said Tan Szue Hann, Head of Sustainability (Real Estate), and Director of ESG Strategy (Fund Management) at Keppel Ltd. Keppel Bay Tower, Singapore’s first net-zero office building, exemplifies this with efficient air handling, smart lighting, improved air quality, and tenant engagement, boosting sustainability and long-term occupancy.

“Keppel will not just take on a new tool or a new piece of technology because it’s required, there has to be a certain efficiency in it, and there has to be a certain value that’s created as well,” Tan said.

Sustainability in Building Design and Retrofitting

Environmental responsibility is key to ESG, but real impact requires going beyond compliance. Firms must balance regulations with proactive measures like green certifications, carbon reduction and energy-efficient retrofits.

Research and development in carbon capture and nature-based solutions underscore the need for tech-driven approaches, An highlights. Singapore, in particular, faces unique sustainability challenges due to heat, land scarcity and limited renewable energy options. Rising temperatures and cooling demands require energy-efficient solutions such as adding fans to improve ventilation alongside air conditioning and adoption of paint with cooling and purifying effect.

She advocated that Nature-based solutions will be the way forward as climate crisis cannot be resolved without tackling nature crisis.

Tan cites Seoul’s INNO88 tower as a model for sustainability-driven retrofitting. New urban regulations required removing three floors, but a conscious decision was made to retain the majority of the building’s structure, leading to a retrofit that preserved 30,000 tons of embodied carbon, while cutting operational energy use by 30%, saving SGD 1 million annually. The upgrade also boosted the building’s valuation, attracting investors.

SC Capital Partners applies Building Information Modelling (BIM) across all data centre developments under its SC Zeus platform, Ou notes. BIM is critical for optimising energy use and reducing waste—both key in energy-intensive assets like data centres. While adoption in Asia remains uneven, including in Japan and South Korea, the firm has made BIM a baseline requirement to support stronger ESG and operational outcomes from day one.Tan cites Seoul’s INO88 tower as a model for sustainability-driven retrofitting. Heritage regulations required removing three floors, leading to a retrofit that preserved 40,000 tons of embodied carbon and cut energy use by 30%, saving SGD 1 million annually. The upgrade also boosted the building’s valuation, attracting investors.

The future of ESG in real estate hinges on balancing governance, social impact and sustainability. Technology drives efficiency and compliance, but the real value comes from turning data into action. As the industry evolves, ESG must stay at the forefront—ensuring profitability, resilience, and a healthier planet for future generations.

Overall: REITs are providing some relative shelter from the tariff storm. The business of REITs is more domestic in nature than most of the other sectors. Lower interest rates will likely benefit the sector, and the JPY tends to strengthen when financial markets suffer. We continue to view Asian REITs as defensive and under owned.

Japan: JREITs and Developers, despite suffering from the tariff sell-off, have outperformed. We expect defensive sectors to start outperforming, with JREITs taking the lead over Developers. Second quarter reporting will affect the sector in Japan as well.

Australia: Australia has had the largest correction in Asia Pacific (-13% YTD), mostly on Goodman (GMG) due to its size in the index. Overall, sell-off in Data Centers might be overdone, and we believe RBS is poised to continue easing as well. We remain optimistic in other sectors with a preference for living stocks. The Abacus Storage King and National Storage story is developing and should be navigated carefully. We would not be surprised to see more consolidation in the AREIT sector among smaller names.

Hong Kong & Singapore: Despite sharp falls in HK due to Chinese trade tariff retaliation, we see several drivers to support the HK REIT sector. HK Stock Connect should include HK REITs soon (Link REIT and Fortune REIT likely inclusions). We prefer REITs over Developers in HK currently, but could see recovery in both. Anticipated stimulus from Chinese Government to offset tariffs could improve HK sentiment. Singapore REIT (SREIT) sell-off due to trade war presents a good opportunity as falling rates have led to positive refinancing rates and acquisition cycle could restart. Rotational buying in Singapore out of large cap banks could be a tailwind for SREITs as well.

India’s Real Estate Investment Landscape: FY25 Outlook

India’s capital markets continue to evolve, backed by strong macroeconomic fundamentals, policy reforms, and a resilient appetite from both domestic and global investors. The real estate sector remains a key focus, with heightened activity across income-generating and emerging asset classes. With stable demand, strategic capital deployment, and increasing institutional interest, FY25 is poised to be a defining year for the Indian investment landscape.

Key highlights of the report include:

India Market Overview

Robust investment activity observed across core commercial office assets and the industrial & logistics sector.

Emerging interest in data centres and alternative assets, driven by digitisation and rising demand for specialised infrastructure.

Rising participation from global investors in large-scale platform deals and structured equity transactions.

Continued interest in income-yielding assets and Grade A developments across top metros.

Capital Trends & Deal Activity

Strategic partnerships between institutional investors and developers drive capital inflows.

Notable transactions include deals in Mumbai, Bengaluru, NCR, and Hyderabad across office and warehousing sectors.

Increased focus on structured transactions and forward purchase models.

Outlook

Investor sentiment remains positive, underpinned by India’s growth trajectory and real estate sector resilience.

Policy support and infrastructure development expected to further enhance market depth and transparency.

India continues to attract long-term capital seeking stability, scale, and sustainable returns.

The Japanese economy is stagnant but not in recession due to decline in demand caused by rising prices and slowdown in recovery of the Chinese economy.

The market for for-sale real estate in Japan has recovered from the sudden slowdown caused by the impact of COVID-19, and the supply-demand balance has been barely maintained due to decline in demand caused by rising prices and decrease in supply accompanying rising costs despite rising interest rates.

Hotels and retail properties in Japan continue to thrive following recovery from slowdown due to the impact of COVID-19, as the weak yen attributable to differences in monetary policy and other factors has stimulated inbound demand.

In the rental market for office buildings in Japan, vacancy rates continue to decline slowly, and rents continue to rise gradually with some exceptions.

Although transaction prices have been maintained, both the number of transactions and their amounts are slumping due to a decline in properties for sale, with some investors turning to a cautious stance.

Comparing the economic growth rates and inflation rates of major advanced countries and developing countries, the former show similar fluctuations depending on the country and time period, while indicators for the later show diverse trends.

Among the economic growth and inflation rate indicators of advanced countries, only Japan’s inflation rate shows a clear downward shift.

Among the major countries compared, Japan‘s population has been on a long- term downward trend as natural decrease has not been fully compensated for by social increase.

The populations of major countries continue to grow due to social growth, but the US population is thought to be rapidly increasing, including through illegal immigration, and the economic growth rate is expected to be swinging upward significantly.

Kemmu Kawai joined Longevity Partners Japan in September 2022 as the Country Director. Based in Tokyo, he oversees all operations and activities in Japan, the Asia-Pacific region and beyond. He brings him more than 16 years of experience in finance where he specialised in real estate and credit investments. Before joining Longevity Partners, he served as a Portfolio Manager at Norinchukin Bank and as Investment Manager at Center Point Development.