John Lim on Purpose, Partnership, and the Future of Asia’s Real Assets

Inside the mind of the APREA Chairman as he reflects on leadership, long-term value, and shaping resilient capital markets across the region.

This article is an excerpt from the the white paper “Sustainability-Linked Insurance: Rewarding Climate Risk Adaptation” co-published by Link Asset Management, AXA and Marsh.

For decades, the real estate industry has viewed insurance as a necessary cost of doing business — a safeguard against unforeseen risks, but rarely a tool for creating value.

That paradigm is shifting.

Link Asset Management (Link) has introduced how real estate climate resilience efforts can be linked with insurance terms — a model that doesn’t just provide protection but actively rewards investment in climate adaptation measures.

By quantifying climate risk and making targeted resilience investments, Link, through its insurance broker Marsh Hong Kong, secured an 11.7% reduction in property insurance premiums — significantly outperforming the industry’s ~3% average. Even more importantly, Link negotiated an additional 7.5% premium reduction tied to its loss ratio, creating a direct financial incentive to continue investing in long-term climate preparedness.

This case study isn’t just about one company’s success. Rather, it highlights a fundamental shift and real-time opportunity for real estate firms — and insurers — to align incentives and build climate resilience.

From Risk Awareness to Resilience in Action

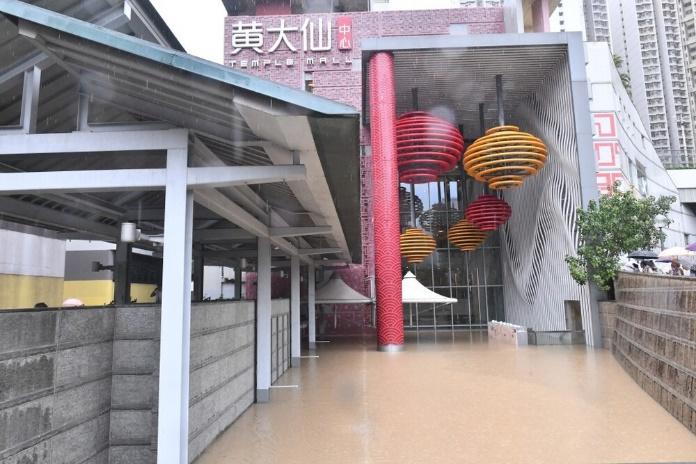

Extreme weather events are no longer an anomaly — they are an operational reality. In September 2023, Hong Kong experienced a “double whammy” of Super Typhoon Saola and record-breaking black rainstorms, causing widespread property damage. The conventional response across the real estate industry was reactive: filing claims, absorbing losses, and bracing for inevitable premium hikes.

Link chose a different approach. Rather than treating resilience as a cost, it saw an opportunity for investment — one that could be quantified, optimised, and ultimately rewarded.

Link reframed its relationship with insurers from a transactional one to a partnership in risk management:

By integrating risk identification, targeted mitigation, and transparent insurer engagement, Link transformed resilience from a defensive measure into a financial advantage.

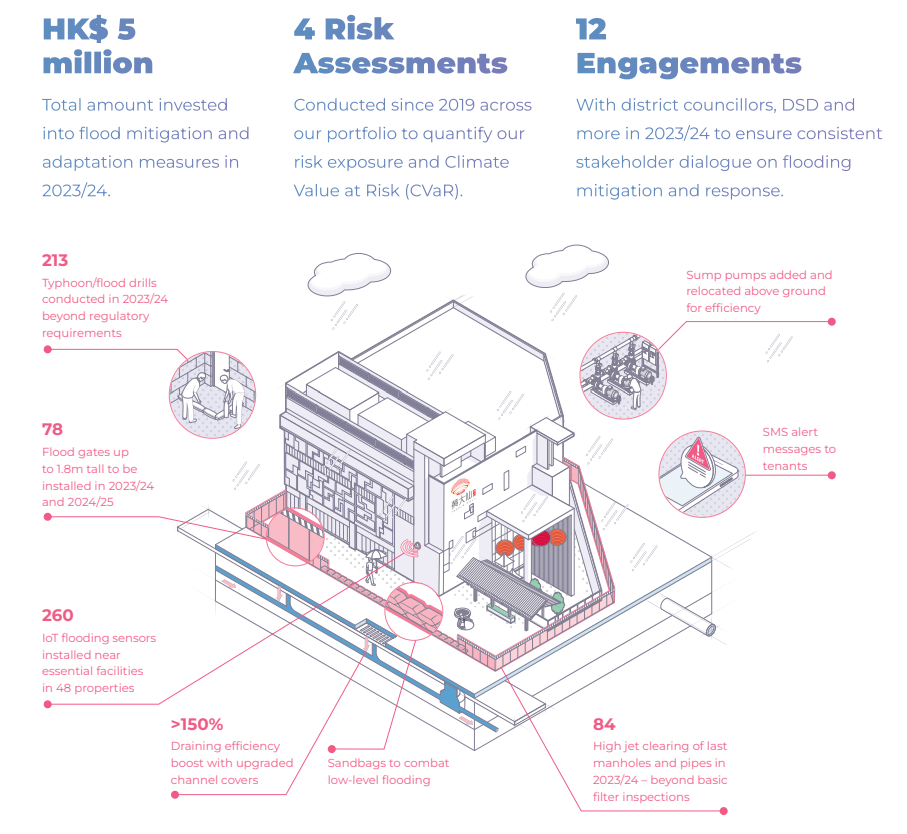

The Resilience Framework: Six Pillars of Climate Adaptation

Building a resilience-linked insurance model requires a structured, data-backed approach. Link’s framework consists of six interconnected pillars:

Each of these pillars feeds into Link’s resilience-linked insurance structure, ensuring measurable risk reduction, operational stability, and long-term financial savings.

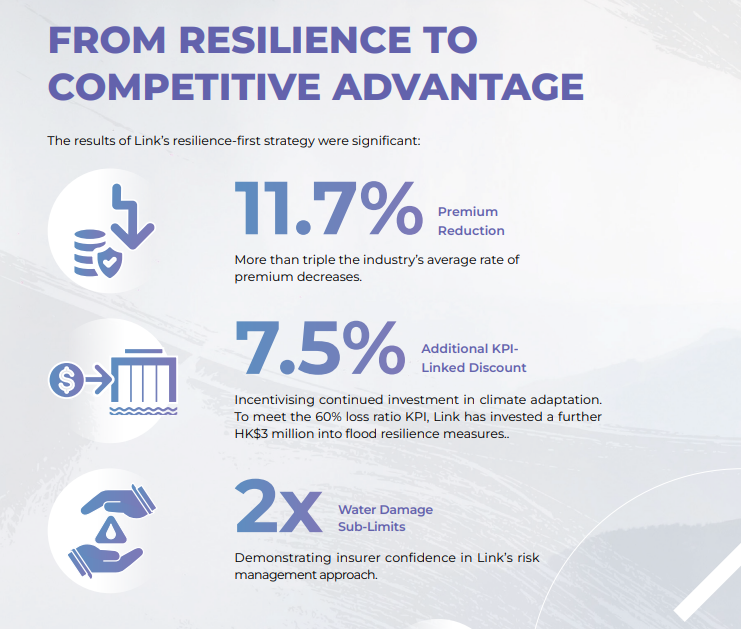

From Resilience to Competitive Advantage

The results of Link’s resilience-first strategy were significant:

By embedding climate resilience into its operational and financial strategy, Link has proven that climate adaptation isn’t just a defensive measure — it’s a value driver.

“We welcome the efforts made by Link REIT to make their assets more resilient and sustainable, and are pleased to show our support through promising insurance capacity and T&Cs. Extreme weather and climate risk are real issues for real estate and best tackled when all stakeholders work together.”

– Quoted by one insurer on an anonymous basis

What’s next?

Real estate is at a crossroads. Rising climate risks will continue to challenge traditional insurance models, but Link’s resilience-linked insurance structure offers a replicable blueprint for other asset owners.

The shift from reactive insurance to proactive risk management has begun — who will follow?

Addressing Scope 3 emissions has become increasingly vital in real estate, driven by rising expectations from investors, regulators, and stakeholders for meaningful climate action. According to the World Green Building Council, buildings account for around 39% of global energy-related carbon emissions. Of this total, around 11% is attributed specifically to embodied carbon emissions, which arise from materials and construction. With the building operational efficiencies continuously to be improved and electricity grids to be decarbonised, embodied carbon emissions represent a progressively larger proportion of total emissions. Hongkong Land has a long history of enhancing energy efficiency and reinvesting in existing assets, Scope 3 emissions represent nearly 90% of our total emissions. As a developer and owner of buildings, prioritise initiatives to address embodied carbon measurement, monitoring and reduction along the supply chains is crucial.

Hongkong Land’s Commitment to Scope 3 Emissions Reduction

Our 1.5°C aligned near-term science-based targets is to reduce 22% carbon intensity for Scope 3 greenhouse gas emissions by 2030. As the first Hong Kong-based developer to create bespoke embodied carbon assessment tools. These tools adopt a supplier-based approach to estimating emissions and provide a level of granularity. Hongkong Land integrates these across project design, tendering, and construction. The company actively collaborates with industry partners to standardise procurement guidelines, focusing specifically on five key construction materials: cement, concrete, façade, rebar, and structural steel.

Case Sharing on New Development in Shanghai

Hongkong Land’s Westbund Central is the Group’s largest-ever single investment, it is an US$8 billion development encompassing approximately 1.1 million sq. m. of prime mixed-use property strategically located at Shanghai’s Xuhui Waterfront. Westbund Central demonstrates Hongkong Land’s proactive and strategic approach to embodied carbon management. Utilising our bespoke embodied carbon assessment tools, the project team systematically measures the embodied carbon intensity associated with the development. The team closely reviews construction materials and actively pursues opportunities to minimise embodied carbon through targeted optimisation efforts. By applying detailed schematic design analyses and structural material optimization techniques, the project has already achieved significant reductions. Specifically, these optimisation strategies have resulted in a achieving a 16% overall carbon reduction in structural steel and a 7% in concrete.

Westbund Central, China

Case Sharing on Transformation of LANDMARK in Hong Kong

Hongkong Land’s Tomorrow’s CENTRAL project, a plan to invest over US$400 million by expanding and upgrading its LANDMARK retail portfolio over a three-year period, has established an ambitious target to divert at least 75% of total construction waste by weight from landfills. Before commencing refurbishment works, we conducted a comprehensive pre-refurbishment audit, systematically assessing and analysing the waste likely to be produced from demolition activities. The audit provided a clear, quantitative overview of anticipated waste streams and identified actionable opportunities for reclaiming, reusing, and recycling materials, guiding contractors to maximise resource recovery and circularity.

We identified 15 major construction materials and products including concrete, glass, wood, metal, and others for prioritised reuse, circular recycling, and diversion from landfills. By integrating circular economy principles, the project reduces demand for new raw materials, diminishes waste disposal volumes, and significantly lowers embodied carbon emissions associated with material extraction, manufacturing, transportation, and disposal.

LANDMARK ATRIUM, Hong Kong

Conclusion

Through these targeted initiatives and strategic actions ranging from bespoke embodied carbon assessment tools and structural design optimisation at West Bund, to comprehensive pre-refurbishment audits and circular material reuse strategies in Tomorrow’s CENTRAL. Hongkong Land demonstrates a robust and proactive approach to reducing embodied carbon emissions. We will continue to make significant strides towards sustainability targets 2030.

Kemmu Kawai joined Longevity Partners Japan in September 2022 as the Country Director. Based in Tokyo, he oversees all operations and activities in Japan, the Asia-Pacific region and beyond. He brings him more than 16 years of experience in finance where he specialised in real estate and credit investments. Before joining Longevity Partners, he served as a Portfolio Manager at Norinchukin Bank and as Investment Manager at Center Point Development.

Kemmu Kawai

Managing Director

Longevity Partners