Rebounding Asia Pacific: Conference Takeaways from the Asia Pacific Real Assets Leaders’ Congress 2023

Read the highlights and takeaways from APREA’s flagship conference, the Asia Pacific Real Assets Leaders’ Congress 2023, which featured the best and the brightest in the industry.

Despite global challenges, optimism prevails for Asia Pacific’s growth, presenting opportunities in both public and private markets. Key takeaways include the region’s commitment to sustainability driving investment opportunities, discussions on infrastructure financing challenges and opportunities, insights into traditional vs alternative assets, the impact of rising interest rates on REITs, and the evolving landscape of family offices.

The Business Case of Embracing ESG – A CDL Case Study

2023 is set to be the hottest year since records began in the mid-1800s. The Swiss Re Institute further warns that without climate action, the world economy could shrink by 18% in the next 30 years. Asian economies are particularly vulnerable – with China at risk of losing almost 24% of its GDP under the most severe climate scenario. In contrast, these figures can lessen and be as low as 4% if the 2015 Paris Agreement targets are met.

The cost of inaction is greater than the cost of action. With societal demands for ethical and responsible business practice intensifying, consumers, investors, and employees are increasingly scrutinising companies’ ESG (environmental, social and governance) performance, favouring those that prioritise environmental stewardship, social responsibility, and sound governance.

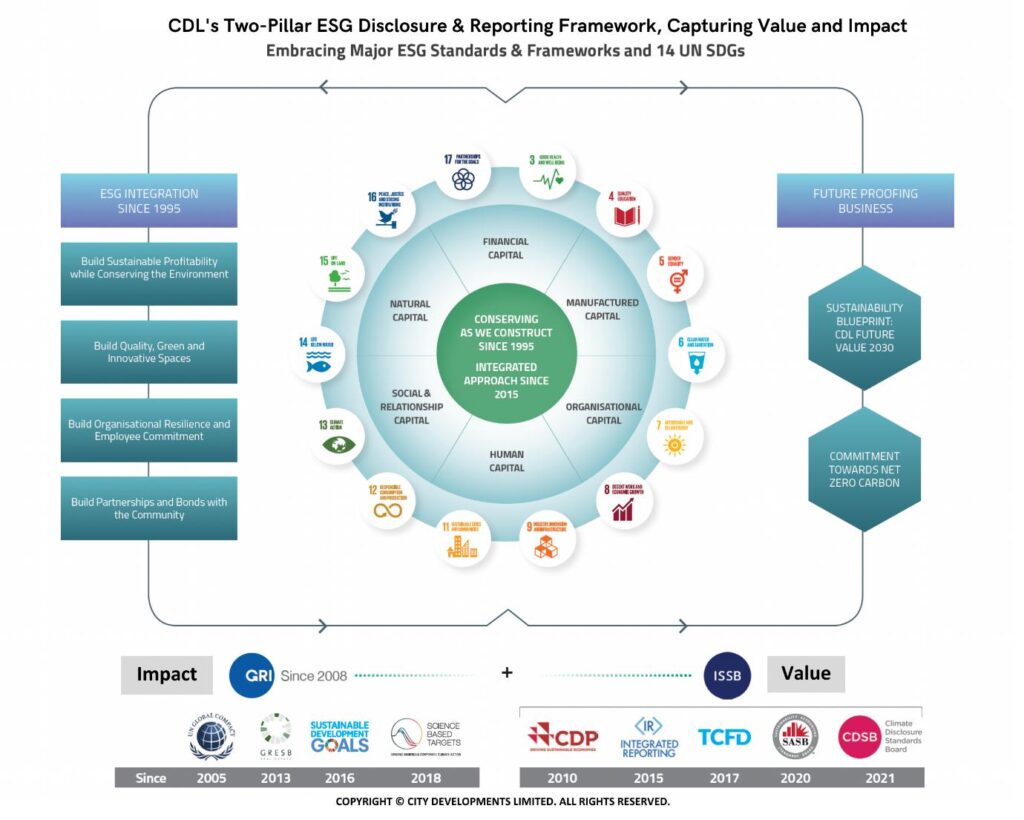

City Developments Limited (CDL)’s ESG strategy and firm commitment to “Conserving as We Construct”, established in 1995, has positioned the company well in the transition towards sustainable business operations. Its value creation business model anchored on four key pillars — Integration, Innovation, Investment, and Impact – provides the company with a solid foundation to mitigate and adapt to unprecedented threats and challenges. With long-standing board and leadership commitment and stakeholders’ support, CDL has remained effective in achieving three deliverables: “Decarbonisation”, “Digitalisation and Innovation” and “Disclosure and Communication”.

Integrating Sustainability into a Company’s Governance Structure, Strategy and Operations

In 2012, CDL established a dedicated Corporate Social Responsibility (CSR) and Corporate Governance comprising independent directors, to provide strategic direction and oversight of its ESG activities. In 2016, the committee was renamed Board Sustainability Committee. The committee ensures that ESG considerations are embedded within CDL’s corporate strategy and decision-making processes.

CDL’s integrated sustainability governance structure that extends both horizontally between the ESG pillars and functions and vertically across hierarchical levels up to the Group CEO and the Board

Effective corporate governance includes putting in place essential policies and guidelines across the organisation. To enhance transparency, CDL’s corporate policies and guidelines are publicly available on its corporate website, sustainability microsite and staff intranet.

Innovation and Investment: Harnessing Green Technologies and Sustainable Financing

Climate and social risks are business and investment risks. As demand for green financing grows, companies with strong ESG performance will gain better access to fast-growing ESG investment funds. In 2022, CDL established its Sustainable Investment Principles to govern ESG factors in investment decisions, aligning CDL’s investments with its commitment towards a low-carbon future.

Building a green and low-carbon future is not possible without smart and innovative solutions. In 2020, CDL set up Green Building, Decarbonisation and Safety team to play a pivotal role in driving innovation and investment. The team identifies and implements cutting-edge technologies and solutions to reduce CDL’s carbon footprint in construction, operations, and asset management.

Impact: Setting targets, tracking, and disclosing ESG performance

Companies can only manage what they measure. As the first Singapore company to publish a dedicated sustainability report since 2008, CDL has benefitted from the hands-on experience of producing 16 sustainability reports to-date. Using a unique blended reporting model harmonising key and relevant international reporting frameworks, standards, and approaches with the GRI Standards at its core, CDL has been able to identify material issues, set targets, track performance, and improve deliverables. This has enabled its management to take strategic and prompt action to improve, generate positive impacts and future-proof its business.

CDL’s Value Creation Model, a unique blended two-pillar sustainability reporting framework that harmonises nine key ESG reporting standards and 14 UN Sustainable Development Goals

Looking ahead, the global race to zero will continue to exert pressure on countries and companies to accelerate climate action. Sustainability-related risks and opportunities will likely increase as social, political, and cultural attitudes continue to evolve. The integration of ESG into a company’s corporate strategy is thus critical for sustained value creation.

CBRE professionals in Asia Pacific observe that investor risk appetite remains low amid a delayed recovery in investment activity. A majority of respondents expect a recovery from Q2 2024 onwards, amid limited expectations of interest rate cuts in the first half of 2024.

Selling pressure persists across most of the region, with the primary exception of India which is receiving increased buying interest from investors. Most investors – excluding private investors and institutional investors/LPs – also have higher intentions to sell than in Q1 2023.

The survey reveals that the price gap is widening for assets with strong fundamentals, such as multifamily, institutional-grade modern logistics facilities, prime shopping malls, cold storage and data centres.

While institutional-grade logistics remains the most popular sector for investors, interest in retail has increased. Slow re-pricing is prompting investors to seek alternative or niche sectors, with real estate debt strategies gaining traction among alternatives.

Cap rates are set to expand across Asia Pacific, reflecting a prolonged high interest rate environment, and as re-pricing lags behind the US and Europe.

Asia Pacific Glide Path Report (Cushman & Wakefield)

What we know is that the global commercial real estate (CRE) sector, like many sectors, faces significant near-term headwinds. In Asia Pacific, while the economy remains resilient, the CRE investment market is in the middle of a reset given interest rate uncertainty, tighter lending conditions, and a challenging global environment. However, we also know that the CRE sector will recover. In fact, historically, the strongest vintage years in terms of CRE returns are the ones that follow periods of dislocation and financial stress.

This report provides a glide path from here to there. That path will not be without challenge; it is therefore just as important to address the near-term challenges as it is to conceptualise the path to clear(er) skies. Our approach to investing is predicated in part on positioning for the future and not missing out on thematic and demographics that will drive Asia Pacific in the next decade.

Reworking The Office Asia Pacific (Cushman & Wakefield)

The office sector is currently going through global structural change as organisations seek to adapt their physical spaces to new ways of working and adjust their corporate real estate decision making. Our ‘REWORKING’ series examines decision-making for occupiers under four key considerations: Cost, Carbon, Culture and Community – under which the changing demands, needs and impacts on office spaces and strategies can be examined.

Asia Pacific Data Centre Construction Cost Guide (Cushman & Wakefield)

The guide tracks 37 key data centre locations across Asia Pacific with a comprehensive breakdown of costs covering land acquisition, advanced land clearance and demolition works, base build and fit-out construction costs. It offers a comprehensive analysis of the Asia Pacific data centre landscape, including key trends that are shaping the region’s data centre sector. This is the first year that Cushman & Wakefield has published its data centre development cost data.

Hiking Sustainability via Walkable Cities (Cushman & Wakefield)

The urban area and its associated design, planning, development and operation, plays and will continue to play a big role in bringing transformational change to address the changing way we live as well as our changing climate. To bring about beneficial living and urban environmental sustainability change that results in sustainable urban environs, in this report we will look at the following topics:

A Change for the Good

The 15-Minute City

Urban Public Space

Transit-Orientated Development

Ecological Solutions

Net-Zero Buildings

Key Takeaways

To hike sustainability and bring about beneficial urban environmental sustainability change that results in walkable sustainable urban environs, one concept cities in Asia Pacific can look to adopt and implement is the ‘15-minute city’ concept.

The 15-minute city is a fresh concept that promotes both urban environmental sustainability and urban livability.

When specifically considering urban public space in the Asia Pacific region in relation to sustainable 15-minute city urban environs, the aim for local governments is to generate all-inclusive citizen-friendly settings that are also economically workable.

To interconnect sustainable 15-minute urban environs, it is essential for cities in general, including those in Asia Pacific, to have a well-planned and efficient overall public transport system that is easily accessible, is convenient and cuts both journey times and air pollution levels for all their citizens.

The 15-minute city concept also places much emphasis on the need for greater food production via urban agriculture.

Finally, in order to reduce the amount of energy used by, and carbon emissions from, buildings in the Asia Pacific region, including buildings in walkable 15-minute city precincts, it will additionally be important to take the next step and go carbon neutral, which requires a “carbon balance” to be established.

The Evolution of E-commerce and its Impact on Singapore Logistics Real Estate (CBRE)

Singapore’s retail e-commerce market is projected to grow at a 9.9% CAGR from 2022 to 2027, from S$5.8 billion in 2022 to a size of S$9.2 billion in 2027. Emerging trends such as shopping festivals, live selling and online grocery shopping have presented unique challenges for businesses in managing their logistics supply chain. With the adoption of omnichannel retail models and the outsourcing of last mile deliveries to 3PLs, the need for strategically located warehouses becomes paramount.

This report seeks to explain how the logistics sector is positioned to capture e-commerce demand, as well as potential recommendations for landlords and occupiers as they seek to future proof their logistics real estate portfolio.

Can the sustainability tech boom help decarbonize real estate? (JLL)

With carbon reduction deadlines looming and regulations tightening, more businesses are adopting fast-evolving technologies to measure, monitor and manage their emissions and guide future sustainability decisions.

Sustainability technologies will account for the biggest share of increased tech budgets for both occupiers and investors over the next three years, according to JLL’s survey of 1,000 companies. Over two thirds of occupiers say tech that helps them to manage and report on their sustainability progress is a top budget priority.

Globally, 45% of occupiers and 62% of investors surveyed plan to adopt energy or emissions management tech in the coming year. Another 62% of investors are interested in tech that supports sustainability monitoring and reporting while evaluating climate risk in portfolio planning is an emerging area.

“Tech is a critical enabler for companies to better understand how they’re doing in terms of their net zero goals through from flagging risks in their portfolio to monitoring their day-to-day operations,” says Ramya Ravichandar, Vice President, Technology Platforms – Smart & Sustainable Buildings at JLL.

“There’s now a mature market to address companies’ sustainability reporting and management needs and ensure they can comply with incoming public disclosure regulations such as California’s new Climate Corporate Data Accountability Act.”

Kemmu Kawai joined Longevity Partners Japan in September 2022 as the Country Director. Based in Tokyo, he oversees all operations and activities in Japan, the Asia-Pacific region and beyond. He brings him more than 16 years of experience in finance where he specialised in real estate and credit investments. Before joining Longevity Partners, he served as a Portfolio Manager at Norinchukin Bank and as Investment Manager at Center Point Development.