The new PMRE Monitor 2024: An AI User Manual provides assistance and offers guidance on the path to the future. The results of the market analysis have been used to create a handbook – an AI User Manual – that prepares players of the real estate industry for the use of AI.

You will learn in detail

which visions can be realised with AI in the real estate industry,

how employees can be mobilised to use AI and

how the transformation of the entire company can be managed.

2024 Asia Pacific Real Estate Market Outlook (CBRE)

High interest rates, a slow recovery in mainland China and geopolitical tension weighed on the Asia Pacific real estate market in 2023. While these concerns are set to persist into 2024, CBRE expects an upturn to commence by mid-year.

From an economic perspective, the U.S. economy is poised for a soft landing in 2024, and the downward interest rate cycle in Asia Pacific is expected to commence mid-year.

The office market will continue to witness a supply boom and occupiers will leverage the higher availability to drive flight to quality and workplace optimisation. Prime office and green space will see growing demand.

In the retail space, despite a cautious approach to CapEx and store network planning, retailers are poised to capitalise on favourable market conditions to upgrade and expand.

Logistics occupiers’ appetite for expansion is expected to moderate further, and occupiers will give closer scrutiny to real estate plans and capital expenditure.

Expectations are that while hotel ADRs should normalise in most markets, occupancy growth in well-managed assets should drive revenue growth.

Commercial real estate investment is expected to remain muted in H1 2024. However, H2 2024 will see an uptick in investment activity on the back of re-pricing and interest rate cuts.

Asia Pacific Cap Rates Report | Q4 2023 (Colliers)

There are signs that interest rates have peaked in some markets in APAC with expectation on more market activities and a gradual recovery in 2024.

The APAC real estate sector was experiencing a low transaction environment in Q4 2023. Owners, investors, and occupiers remained cautious about real estate investments with a lot longer due diligent process. However, the signs of peak interest rate in some APAC markets are resulting a more positive sentiment towards investments in 2024.

Key Highlights in Q4 2023:

Office Sector

Transaction volume continued to be low across all major Australian office markets. The sales that have begun to complete are predominantly secondary grade assets with value-add potential. These sales are primarily being undertaken by syndicates. These transactions require a significant amount of time to complete due diligence and raise the required capital. The further interest rate rise that occurred in November 2023 continues to put pressure on capitalisation rates. The number of assets being listed and subsequently withdrawn due to pricing disconnect between vendors and purchasers suggests that there is still further cap rate softening to come in 2024.

The rental rates for office segment have increased slightly in some micro markets of Bengaluru. This improvement was attributed to the commencement of the Mass Rapid Transit System and the overall improvement in connectivity. However, property values have not moved in tandem due to low transaction volume. As a result, the cap rates on the higher end of the range have decreased.

No en-bloc office sales were transacted in Jakarta last quarter. Office assets along with the new phase of the public light rail transit have triggered investor interest. A huge supply is expected to enter the market. Corporate users have started looking for newly built offices either acquiring the whole building or leasing more space for expansion purposes.

Office demand in Manila remains lethargic and there is an increase in supply pressure with new office buildings coming onto the market.

Retail Sector

Retail has been experiencing a consistently low transaction environment for Australia as the market recalibrates based on the increased interest rate environment. Consumer confidence appears to be falling, impacting non-discretionary spending. We expect further cap rate softening into Q1 and Q2 2024 as the price differences between vendor and purchases expectations continues.

In Bangkok, there were no significant retail transactions in the past quarter to evidence value movements. Retail rents have increased following the opening of some premium malls in core locations, which has pushed the cap rates up slightly. However, the rise in rental value for those premium stock is still yet to be seen whether it will establish a continuing upward trend in the immediate term.

In the fourth quarter, rental rates in prime areas in Beijing and Shanghai have shown improvements. This upturn can be attributed to the resurgence of consumer engagement in these areas. Despite the overall growth in total retail sales, it will take some time for rental rates to fully adjust and align with the improved consumption. Property owners and landlords are taking a cautious approach to rental growth, allowing adequate time for rents to align with evolving consumption patterns and market condition.

The retail occupancy and rental performance in Hong Kong have generally remained healthy, thanks to robust domestic consumption. However, investors exhibit caution towards the retail sector due to its high vacancy rate.

Industrial Sector

Australian industrial market drove the movement in the industrial sector in this survey. The current rental levels are expected to peak in 2024 as a result of tenants’ gross occupancy costs hitting their limit. Nonetheless, vacancy rates are still low across Western Sydney, prime industrial area, which should see rents hold at current levels throughout 2024. However, incentive levels are starting to creep upwards.

The transactions concluded in Q4 have resulted similar cap rates as the last quarter in Jakarta. Major logistic players have been observed looking for land or joint venture partners.

The industrial cap rates remained flat owing to stabilization of yields and asset values as sustained demand from the third party logistic (3PL) players, eCommerce and fast-moving consumer goods (FMCG) sectors is countered by new supply in Mumba

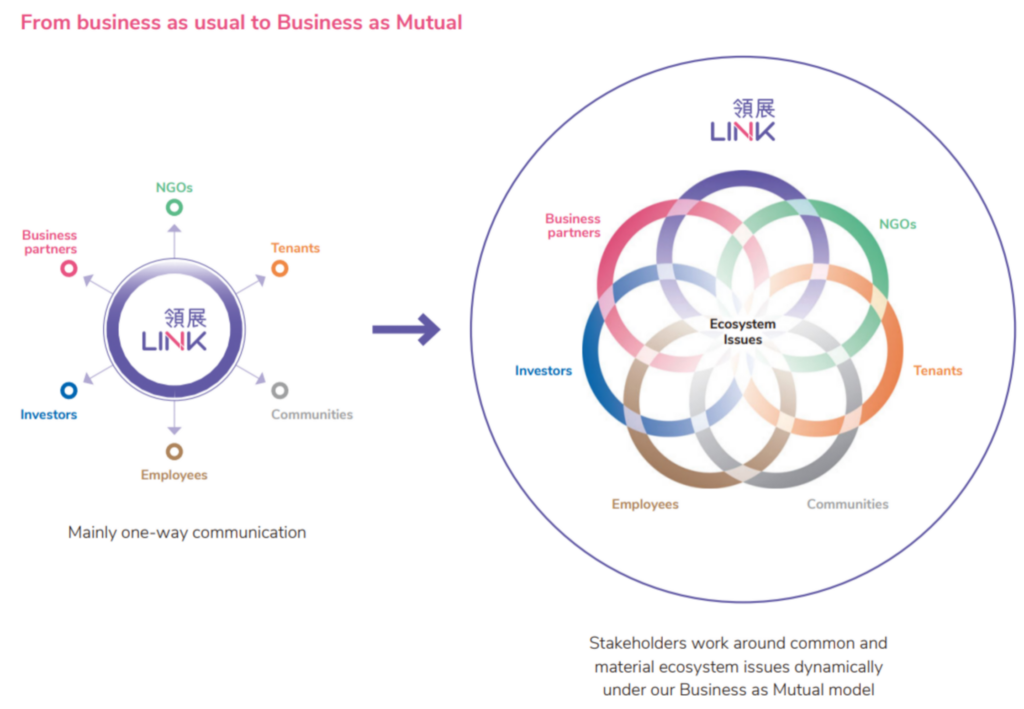

Business as Mutual: A Blueprint for a Sustainable, Future-Fit Business

During the past years, businesses have experienced a series of once-in-a-generation challenges, forcing them to re-evaluate how they operate. From COVID-19 to geopolitical instabilities, these challenges have shown that individual events, activities and decisions all have impacts that cascade throughout a value chain, potentially with global consequences.

The challenges posted by COVID-19 have underscored the true meaning and importance of ‘Business as Mutual’. No man is an island, and no business can act independently. We need to work together in order to thrive. One thing is clear: moving forward, business as usual is obsolete. We must transition to Business as Mutual.

What is Business as Mutual?

Business as Mutual (BAM) is Link’s future-fit leadership mindset and management tool designed to achieve long-term business sustainability through dynamic engagement with stakeholders.

BAM positions Link and other stakeholders as an ecosystem, in which all stakeholders coordinate and align efforts to address common material issues instead of Link-centric topics alone.

This approach is critical to maximise value creation and build a resilient ecosystem where our business, stakeholders and the community can work together on common and material ecosystem issues collaboratively.

Not only is this good for Link but it also contributes to creating ecosystem-wide shared value for all stakeholders, such as better economic performance, environmental resilience and social inclusion.

We apply the BAM approach throughout our business, including our approach to sustainability. For any project we execute or ecosystem issue we try to address, we actively engage with and collaborate with our stakeholders to inform and evolve our thinking and decisions.

Integrating BAM at Link

Over the years, we have implemented BAM in multiple areas of our business to help our stakeholder ecosystem flourish. Below are just a few examples:

CONNECTION: an annual ESG stakeholder engagement event to share challenges and solutionsStakeholder engagement workshops for our new community mall at Anderson Road QuarryFood Angel’s We Link We Share Programme sponsored as a project under Link Together Initiative

What’s Next?

As risks and opportunities emerge in a “new normal” environment and broader societal expectations shift, we believe BAM will become more essential than ever in helping our stakeholders and partners achieve long-term ecosystem sustainability.

Going forward, Link will continue to evolve the BAM approach, from strengthening internal governance for BAM to developing a range of tools, metrics and methodologies to accelerate the transformation.

Dr Calvin Lee Kwan

Managing Director – Sustainability and Risk Governance Link Asset Management Limited

The Global Real Estate DEI Survey is the only corporate study of diversity, equity and inclusion (DEI) management practices and data benchmarking in the commercial real estate (CRE) industry.

This third iteration of the Global Real Estate DEI Survey is the result of the collaboration between six sponsoring associations NAREIM, NCREIF, PREA, REALPAC, ULI and Ferguson Partners, as well as 14 supporting associations AFIRE, AIA, APREA, AREF, BOMA, BPF, CFMA, CoreNet Global, CREFC, EPRA, NAIOP, OSCRE, PFA and RICS.

This is a summary report of high-level results providing a view of DEI metrics relating to:

DEI program structure, resources and ownership.

Policies focused on recruitment, retention and promotion, inclusive culture, tracking and accountability, and pay equity.

Employee demographics by gender and race/ethnicity, across seniority and job function, as well as DEI hiring, promotion and

departure trends year-over-year.

Survey participants receive a spreadsheet with full data, providing for an in-depth look and suitable for benchmarking DEI policies and achievements against peers.

The Global Real Estate DEI Survey Volume III represents 296,902 full-time real estate employees, $1.98 trillion of assets under management, and a cross-section of the commercial real estate industry in terms of size, region and business classification.

The Survey brings together participation from 216 unique organizations which provided 236 submissions detailing their DEI practices in North America (79.2% of respondents), Europe (11.9%) and Asia-Pacific (8.9%). Data was collected between July 17 and September 29, 2023.

As we embark on a new year, the Asia Pacific real assets industry stands at a crossroads, shaped by the challenges of 2023 and the promise of a resilient recovery in 2024. In our latest issue of the APREA Market Flash, we engage industry leaders and experts for their perspectives on key trends and strategic considerations that will define the outlook for the region. Our questions revolve around these topics:

Key Trends Shaping 2024: Reflecting on the challenges and opportunities arising from the uncertainties of the past year, we delve into the trends that will be pivotal in steering the real estate market toward a path of recovery.

Portfolio Configuration for 2024: As the global and regional economic landscapes continue to evolve, configuring portfolios becomes a strategic imperative. We explore how investors plan to navigate exposure to the Asia Pacific and the rest of the world. Specific countries and sectors within the APAC region are scrutinized to unveil potential hotspots and growth opportunities.

Themes Guiding Strategies: Beyond immediate market dynamics, we probe into the overarching themes that resonate with investors’ strategies in 2024. From the growing demand for logistics space to the flight to quality in the office sector, our experts shed light on the thematic considerations shaping their investment decisions.

Leveraging Private Credit Opportunities: With economic uncertainties and high interest rates looming, the role of private credit in the investment landscape gains prominence. We inquire into how investors can strategically leverage private credit opportunities and explore new asset classes in the Asia Pacific.

2024 Asia Pacific Investor Intentions Survey (CBRE)

CBRE’s 2024 Asia Pacific Investor Intentions Survey was conducted in November and December 2023. Over 500 responses were received from participants who were asked a range of questions related to their buying intentions, perceived challenges and preferred strategies, sectors and markets for the coming year.

The survey uncovered persistently weak buying intentions across Asia Pacific, with selling intentions hitting the highest mark since surveys began. Whilst the rate hike cycle has come to a halt in major global markets, investors are waiting for indications that the current repricing cycle has finished before deploying significant amounts of capital.

Investors in most markets (ex. Japan) will therefore continue to adopt a wait and see approach in H1 2024. However, amid growing expectations that the U.S. Federal Reserve will begin cutting rates in H2 2024, and Asia Pacific’s central banks following suit, commercial real estate investment activity should accelerate in the back half of the year.

Other key findings:

Overall investment sentiment is at the expected level of CBRE’s in-house estimates. Despite similar net buying intentions, more than 40% of investors said they would dispose of more assets in 2024 to realise returns and repay debt. The strongest selling intentions were observed in Australia, Singapore and Hong Kong SAR.

The survey revealed that value-added investment strategies will gain momentum in 2024 as investors look to hit target returns in markets where negative carry continues to persist.

Residential assets (especially multifamily and built-to-rent) logged the strongest uptick in interest, particularly among investors considering value-add strategies. Industrial and offices are still the top property type among core investors.

Healthcare assets remain top of mind for investors looking at alternative assets. Real estate debt climbed to second place in this year’s survey, while a greater emphasis on the living sector (retirement living and student accommodation) was observed.

Japan retained its position as the most preferred market for cross-border investment for a fifth consecutive year. Singapore and Australia followed in second and third place, respectively. Investors remain attracted to highly liquid markets with stable income.

Just over 60% of investors, the bulk of which are private equity funds, real estate funds and REITs, intend to retrofit existing buildings to be more sustainable or ESG-compliant in 2024; a trend ensuring value-added strategies are their preferred approach.

Navigating the Real Assets Landscape in 2024: Trends, Challenges, and Opportunities

The evolving landscape of real assets in 2024 reflects a cautious optimism after a year of uncertainty in 2023. From Asia Pacific’s stable cycles offering diversification to critical shifts in logistics and office spaces, the market dynamics are diverse. Investors navigate growth sectors such as new economy, senior housing, and co-living spaces, while private credit opportunities emerge in various markets. Structural shifts, including technology integration and sustainability initiatives, reshape demand trends. Amid global economic uncertainty, strategic flexibility and a focus on growth sectors define the approach for investors in the year ahead.

Asia Pacific Office Outlook 2024 (Cushman & Wakefield)

Cushman & Wakefield’s 2024 Asia Pacific Office Outlook provides supply, demand, vacancy and rent data forecasts for cities in Australia, China, India, Indonesia, Japan, Korea, Malaysia, the Philippines, Singapore, Thailand and Vietnam.

REGIONAL OVERVIEW

Key Messages:

Inflation, though largely improved, remains above target bands in most markets across the region; a ‘higher for longer’ interest rate scenario is anticipated.

Asia Pacific economic growth is expected to slow but to remain in positive territory (3.5% to 4.0% real average annual growth) in 2024.

Despite a weaker economic outlook, regional office demand is forecast to reach pre-pandemic levels in 2024—but above average levels of new supply will drive vacancy higher.

Rental growth is forecast to remain flat in 2024 before slowly accelerating from 2025.

Newer, high-quality buildings are likely to outperform given the ongoing flight to quality.

Against a volatile economic backdrop, the Asia Pacific office market remains steadfast and continues to grow. Approximately 50 million square feet (msf) of Grade A office stock was absorbed across the region’s top 25 cities during the first nine months of 2023, with a further 12 msf expected in the final quarter. Annual office demand in 2023, forecast at 62 msf, is an 11% improvement on last year’s 55 msf.

New supply in 2023 will total 109 msf, outstripping demand and causing vacancy to tick upwards to 17.6% from 16.1% in 2022. Rental growth has subsequently slowed and is likely to be down around 0.5% on a weighted average basis.

The outlook remains broadly skewed to the positive. Demand is forecast to increase to 83 msf in 2024 and to 87 msf in 2025, which would match pre-pandemic performance. However, waves of new supply are also expected, with nearly 235 msf of completions forecast over the next two years to place further upward pressure on vacancy, which is now expected to peak at 18.4% in 2024 and then hold steady through 2025. This will keep downward pressure on rents which are likely to remain flat in 2024, at the weighted regional average level, before slowly accelerating from 2025. Accordingly, the window of opportunity remains open for occupiers over the near term.

Picture this – despite around 43% of the installed power capacity of India being renewable, coal-based thermal power still contributes to almost 75% of its power generation. However, the country is making rapid strides towards achieving its ambitious goal of meeting 50% of its energy requirements from renewable energy by 2030.

The policy push has been strong, taking cues from which prominent real estate developers have begun to take meaningful steps towards attaining their ESG goals. Renewable energy, more often than not, is the first step towards achieving ESG compliance.

Through CBRE India’s first report on renewable energy, we have tried to answer the below questions and more:

What is the current state of renewable energy across India?

What are the policy measures that central and state governments are providing to boost the adoption of renewable energy in the country?

What are the common challenges that corporate occupiers face in adopting renewable energy and how can they overcome them?

What are the different renewable energy options available to corporates and how can they access those?

How are leading office developers in India aligned with sustainable power?

How can corporates achieve their renewable energy goals?

Kemmu Kawai joined Longevity Partners Japan in September 2022 as the Country Director. Based in Tokyo, he oversees all operations and activities in Japan, the Asia-Pacific region and beyond. He brings him more than 16 years of experience in finance where he specialised in real estate and credit investments. Before joining Longevity Partners, he served as a Portfolio Manager at Norinchukin Bank and as Investment Manager at Center Point Development.